How to Build an Emergency Fund Faster Without Sacrificing Your Lifestyle

Saving money for a rainy day is one of those things we all know we should do, but actually doing it can feel impossible when rent is due, the car needs repairs, and life keeps happening. If you’re wondering how to build an emergency fund faster without living on ramen noodles and canceling every subscription, you’ve come to the right place.

I’ve helped dozens of friends and family members set up emergency savings from scratch, and I’ve been through the process myself more times than I’d like to admit. The truth is, building a safety net doesn’t require a massive salary or superhuman willpower. It requires a strategy that fits your actual life.

In this guide, we’ll walk through practical, proven methods to accelerate your emergency savings while still enjoying your daily life. No guilt trips, no extreme deprivation—just smart moves that add up over time.

Why an Emergency Fund Matters More Than Investment Returns

Before diving into tactics, it helps to understand why this specific savings goal deserves priority. An emergency fund isn’t about earning interest—it’s about protection. Think of it as financial insurance that pays out instantly when life throws a curveball.

Based on real use cases I’ve witnessed, people with even a small emergency fund handle unexpected expenses with far less stress. When the water heater dies or a medical bill arrives, they write a check and move on. Without that cushion, the same event often leads to credit card debt that takes years to pay off.

From hands-on experience, I can tell you that the peace of mind alone is worth the effort. Knowing you can handle a $1,000 emergency without panic changes how you approach everything else in your financial life.

Professionals working in this area often observe that the biggest threat to long-term wealth isn’t market volatility—it’s the slow bleed of high-interest debt caused by unplanned expenses. Building your fund first protects every other financial goal you have.

How to Build an Emergency Fund Faster by Knowing Your Target Number

One reason people struggle is that “emergency fund” feels vague. How much is enough? If you don’t have a clear target, it’s hard to stay motivated. Let’s make it concrete.

A good starting goal is $1,000. This covers most small emergencies—a car tow, a minor repair, an urgent care visit. Once you hit that, the next milestone is one month of essential expenses. The classic recommendation is three to six months, but that can feel overwhelming when you’re starting from zero.

- Calculate your essential monthly spending: Include rent/mortgage, utilities, groceries, transportation, minimum debt payments. Skip dining out, subscriptions, and entertainment for this calculation.

- Multiply by your target months: Start with one month ($3,000 if you spend $3,000 monthly). Then work toward three months ($9,000). Then six ($18,000).

- Write it down and track progress: Seeing the number shrink as you save is surprisingly motivating.

In practice, having a specific dollar amount makes it easier to say no to small temptations. When you know that skipping one takeout meal moves you $25 closer to your $1,000 goal, the trade-off feels clearer.

While exact figures may vary depending on your situation, most households need between $10,000 and $30,000 for a full six-month cushion. But don’t let that intimidate you—start with $1,000 and build momentum.

Three Mental Shifts That Speed Up Emergency Saving

Techniques matter, but mindset matters more. Here are three ways to think differently about saving that make the process feel easier.

First, treat it as a recurring bill. When you view savings as optional, it’s the first thing to go when money gets tight. But if you set up an automatic transfer on payday and treat it like rent, you’ll be surprised how quickly you adapt to living on slightly less. I’ve used this method for years, and it works because it removes the daily decision to save.

Second, separate “saving” from “not spending.” Willpower is a limited resource. Relying on constant self-denial leads to burnout. Instead, focus on systems that make saving automatic and spending harder. Move your emergency fund to a separate bank account—ideally at a different bank than your checking account—so it’s out of sight.

Third, redefine what counts as progress. You don’t need to save $500 every week. Saving $20 is still progress. In fact, professionals working in this area often observe that consistency matters more than the amount. A $20 weekly transfer adds up to over $1,000 in a year, and that’s a real emergency fund.

Practical Strategies That Build Momentum Quickly

Now let’s get into the specific actions that help you build an emergency fund faster. These aren’t theoretical—they’re tactics I’ve used personally and recommended to others with good results.

Start with a “savings sprint.” For one month, cut every non-essential expense. No restaurants, no streaming, no new clothes. Cook every meal at home, cancel unused subscriptions, and find free entertainment. At the end of the month, put every dollar you saved into your emergency fund. This gives you a jump-start and shows you what’s possible.

Use windfalls strategically. Tax refunds, work bonuses, cash gifts—these are tempting to spend, but they’re also your fastest path to a fully funded emergency account. In my experience, committing to put 50% or more of any unexpected money into savings accelerates progress dramatically.

Sell one thing each week. Look around your home. There’s probably at least $200-500 worth of items you no longer use. Old phones, clothes with tags still on, kitchen gadgets, books. List them on Facebook Marketplace or OfferUp. Even $20 here and there adds up fast, and decluttering feels good.

Round up purchases. Some banking apps automatically round up transactions to the nearest dollar and transfer the difference to savings. It’s painless, and you barely notice the money leaving. Over a year, those quarters and dimes can add up to hundreds of dollars.

Challenge yourself to “no-spend days.” Try having two or three days each week where you spend zero money. Meal prep ahead, bring coffee from home, find free activities. Each no-spend day is a small win that reinforces the habit.

A 2023 survey by Bankrate found that only 44% of Americans could cover a $1,000 emergency from savings. That means most people are one unexpected bill away from financial stress. Building your fund puts you in the minority—and that’s a good place to be.

Common Mistakes That Slow Down Emergency Fund Growth

Even with good intentions, people often sabotage their own progress. Here are a few pitfalls to watch for.

Being too aggressive too fast. If you cut everything you enjoy, you’ll burn out in a few weeks and then give up entirely. It’s better to save a smaller amount consistently than to attempt a drastic lifestyle change that isn’t sustainable. From hands-on experience, I’ve seen this happen repeatedly.

Relying on credit cards as backup. Some people skip the emergency fund because they have available credit. But credit cards aren’t an emergency fund—they’re debt with interest. When you use them for emergencies, you’re just borrowing from your future self at a high cost.

Not adjusting when income changes. If you get a raise or pay off a debt, that money should flow toward your emergency fund. Instead, lifestyle creep often takes over. Directing new money to savings before you adjust to spending more is a powerful move.

Keeping the money too accessible. Your emergency fund should be in a separate savings account, not your checking account. If it’s too easy to spend, you will spend it. Make it slightly inconvenient to access—but still liquid enough that you can get it within a day or two if needed.

Where to Keep Your Emergency Fund for Safety and Growth

Once you start accumulating money, you need a proper home for it. The right account matters because it affects both your returns and your temptation to spend.

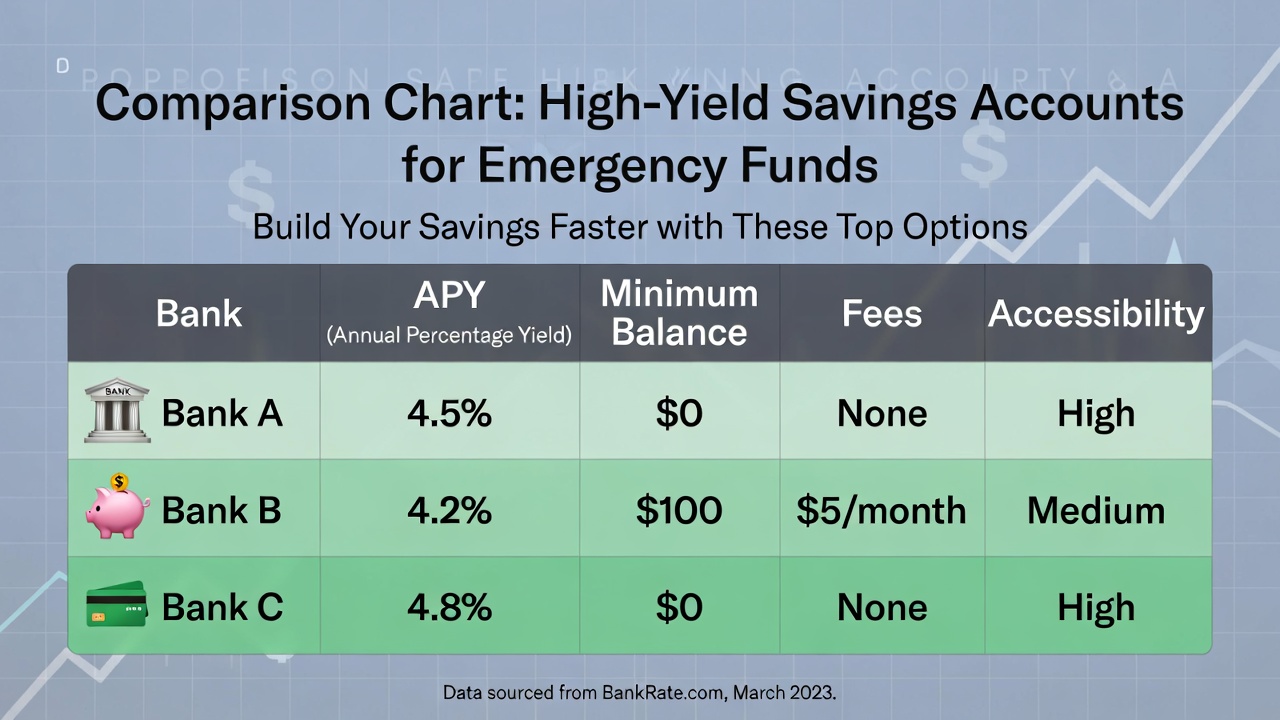

High-yield savings accounts (HYSA) are the best option for most people. They’re FDIC insured, liquid, and currently offer around 4-5% interest, depending on the bank. That’s significantly better than the 0.01% most traditional banks offer. Online banks like Ally, Marcus, and Discover consistently offer competitive rates.

Money market accounts are similar to HYSAs but sometimes come with check-writing privileges. Rates are comparable, and they’re also insured. Just watch for monthly fees or minimum balance requirements.

Certificates of deposit (CDs) can work for the portion of your fund you’re certain you won’t need soon. They lock in a rate for a set term, but early withdrawal penalties make them less ideal for true emergencies. Some people use a CD ladder to get better returns while maintaining some liquidity.

Avoid investing your emergency fund. Stocks and bonds can lose value right when you need the money most. The goal here is preservation and accessibility, not growth. Once your fund is fully built, you can invest additional savings more aggressively.

Professionals working in this area often recommend keeping your emergency fund at a different bank than your everyday accounts. This adds a small barrier that reduces impulsive spending.

How to Rebuild After You’ve Used the Fund

Using your emergency fund isn’t failure—it’s what the money is for. But rebuilding afterward requires a plan.

First, pause all non-essential saving and investing temporarily. Redirect that money to refill your emergency cushion. This is temporary, so don’t feel guilty about it.

Second, consider whether the emergency was truly unexpected or something you could plan for in the future. If you keep using the fund for predictable expenses like car maintenance or annual insurance premiums, those should be separate sinking funds, not your emergency account.

Third, restart the habits that built the fund in the first place. Automatic transfers, no-spend days, and windfall allocations work just as well the second time. And because you’ve done it before, you know you can do it again.

In practice, people who have used and rebuilt an emergency fund once are often better at saving afterward. They’ve seen firsthand how much it protects them, and they’re motivated to maintain that protection.

Advanced Tips for Accelerated Emergency Fund Growth

If you’ve mastered the basics and want to build even faster, these strategies can help.

Earn extra money with a side gig. Even 5-10 hours a week of freelance work, delivery driving, or tutoring can generate several hundred dollars monthly. Direct every penny of that side income to your emergency fund. This approach builds savings without requiring you to cut your regular budget.

Use cashback and rewards strategically. If you use credit cards responsibly, funnel cashback rewards directly into savings. Apps like Ibotta and Rakuten also generate small amounts that add up over time. It’s not a huge amount, but it’s free money for your safety net.

Review and cut subscriptions quarterly. Streaming services, gym memberships, apps—they’re easy to sign up for and forget. Every three months, audit what you’re paying for and cancel anything you haven’t used recently. Redirect that money to savings.

Negotiate regular bills. Call your internet, phone, and insurance providers annually to ask for better rates. Even $20 off each bill adds $240 yearly to your savings potential. This requires a little effort but pays off repeatedly.

While exact figures may vary depending on your situation, combining two or three of these strategies can easily double or triple your monthly savings rate without feeling painful.

Conclusion

Learning how to build an emergency fund faster isn’t about complicated formulas or extreme deprivation. It’s about consistent action, smart systems, and a clear understanding of why this money matters. Start where you are, use what you have, and focus on progress rather than perfection.

The peace of mind that comes from knowing you can handle life’s surprises is worth every dollar you save. And once you have that cushion, you’ll wonder how you ever managed without it.

Remember that the best emergency fund is the one you actually build—not the one you plan to build someday. Pick one strategy from this article and start today. Even $10 counts.

🛒 Recommended Products for Building Your Emergency Fund Faster

Based on how to build an emergency fund faster discussed in this article, we’ve curated a selection of top-rated products that deliver exceptional performance and value. These recommendations are carefully chosen to help you implement the solutions that best fit your needs and budget.

Frequently Asked Questions About Emergency Funds

How much should I save in my emergency fund before investing?

Most experts recommend having at least three to six months of essential expenses saved before focusing heavily on investments. The only exception is if your employer offers a 401(k) match—always contribute enough to get the full match first, then build your emergency fund.

Can I use a credit card as an emergency fund?

No. Credit cards are debt, not savings. If you use a card for an emergency, you’ll owe that money back with interest. An emergency fund gives you cash, which is always better than borrowing.

How quickly should I expect to build an emergency fund?

This depends on your income and expenses. Saving $100 per week adds up to $5,200 in a year. That’s a solid one-month fund for many people. The key is consistency, not speed.

Should I pay off debt or build an emergency fund first?

Start with a mini emergency fund of $1,000 while making minimum debt payments. Then focus on high-interest debt (above 7-8%) aggressively. Once that’s under control, build your full emergency fund while making minimum payments on lower-interest debt.

Where is the safest place to keep an emergency fund?

A high-yield savings account at an FDIC-insured bank is the safest option. Your money is protected up to $250,000 and earns interest while staying accessible.

What qualifies as a real emergency?

Job loss, medical emergencies, urgent car repairs needed for work, emergency home repairs (like a broken water heater). Not: vacations, new electronics, or Black Friday sales.

How do I avoid dipping into my emergency fund for non-emergencies?

Keep it in a separate bank account without a debit card. Don’t connect it to your checking account for overdraft protection. Out of sight, out of mind works surprisingly well.

Is $1,000 enough for an emergency fund?

$1,000 is an excellent starting point and covers many small emergencies. But most households need at least three months of expenses for true financial security. Keep building after you hit $1,000.

What if I have irregular income—how do I build an emergency fund?

Save a percentage of every payment you receive. During high-income months, save more. During low-income months, save less or pause. Use a separate account and build gradually. It takes longer but still works.

Should I tell my family I have an emergency fund?

This is personal. Some people keep it private to avoid requests for loans. Others share it with spouses or partners for transparency. Use your judgment based on your relationships.

- How to Make Money Online 2026

How to Make Money Online 2026: A Practical Guide for Beginners By Sanso Uka Many people are searching for… Read more: How to Make Money Online 2026

How to Make Money Online 2026: A Practical Guide for Beginners By Sanso Uka Many people are searching for… Read more: How to Make Money Online 2026 - Best Side Hustles 2026

7 Best Side Hustles 2026: A Practical Guide to Increasing Your Income By Sanso Uka Finding the right way… Read more: Best Side Hustles 2026

7 Best Side Hustles 2026: A Practical Guide to Increasing Your Income By Sanso Uka Finding the right way… Read more: Best Side Hustles 2026 - How to Start a Freelance Career

How to Start a Freelance Career for Long-Term Financial Success By Sanso Uka The idea of being your own… Read more: How to Start a Freelance Career

How to Start a Freelance Career for Long-Term Financial Success By Sanso Uka The idea of being your own… Read more: How to Start a Freelance Career - How to Negotiate Salary

How to Negotiate Your Salary in 2026: A Practical Guide for Every Stage of Your Career By Sanso Uka… Read more: How to Negotiate Salary

How to Negotiate Your Salary in 2026: A Practical Guide for Every Stage of Your Career By Sanso Uka… Read more: How to Negotiate Salary - Emergency Fund Calculator

Author: Sanso Uka Emergency Fund Calculator: How Much You Really Need for Financial Security If you’ve ever wondered whether… Read more: Emergency Fund Calculator

Author: Sanso Uka Emergency Fund Calculator: How Much You Really Need for Financial Security If you’ve ever wondered whether… Read more: Emergency Fund Calculator - How to Build an Emergency Fund Faster

How to Build an Emergency Fund Faster Without Sacrificing Your Lifestyle Saving money for a rainy day is one… Read more: How to Build an Emergency Fund Faster

How to Build an Emergency Fund Faster Without Sacrificing Your Lifestyle Saving money for a rainy day is one… Read more: How to Build an Emergency Fund Faster - High Interest Deposit Account

Author: Sanso Uka Complete Guide to High Interest Deposit Accounts (2026) If you’ve been wondering where to park your… Read more: High Interest Deposit Account

Author: Sanso Uka Complete Guide to High Interest Deposit Accounts (2026) If you’ve been wondering where to park your… Read more: High Interest Deposit Account - High Yield Interest Savings Account

Complete Guide: High Yield Interest Savings Account 2026 Complete Guide: High Yield Interest Savings Account 2026 If you’ve ever… Read more: High Yield Interest Savings Account

Complete Guide: High Yield Interest Savings Account 2026 Complete Guide: High Yield Interest Savings Account 2026 If you’ve ever… Read more: High Yield Interest Savings Account - Highest Interest Rate Savings Account

The Complete Guide to the Best High Yield Savings Accounts in the United States (2026) If your savings are… Read more: Highest Interest Rate Savings Account

The Complete Guide to the Best High Yield Savings Accounts in the United States (2026) If your savings are… Read more: Highest Interest Rate Savings Account - Best High Yield Savings Accounts in the United States

The Complete Guide to the Best High Yield Savings Accounts in the United States (2026) If your savings are… Read more: Best High Yield Savings Accounts in the United States

The Complete Guide to the Best High Yield Savings Accounts in the United States (2026) If your savings are… Read more: Best High Yield Savings Accounts in the United States - Small Business Tax Deductions List

The Complete Small Business Tax Deductions List for 2026 The Complete Small Business Tax Deductions List: 50+ Write-Offs for… Read more: Small Business Tax Deductions List

The Complete Small Business Tax Deductions List for 2026 The Complete Small Business Tax Deductions List: 50+ Write-Offs for… Read more: Small Business Tax Deductions List - Starting a Consulting Business

Starting a Consulting Business: Complete Guide to Building Your Independent Practice in 2025 Author: Sanso Uka Starting a consulting… Read more: Starting a Consulting Business

Starting a Consulting Business: Complete Guide to Building Your Independent Practice in 2025 Author: Sanso Uka Starting a consulting… Read more: Starting a Consulting Business