Emergency Fund Calculator: How Much You Really Need for Financial Security

If you’ve ever wondered whether you have enough money set aside for a genuine emergency, you’re not alone. Figuring out that magic number can feel confusing, and generic advice like “save three to six months of expenses” often leaves people scratching their heads. That’s exactly where an emergency fund calculator becomes your best financial friend. It takes the guesswork out of the equation and gives you a personalized savings target based on your actual life.

Think of an emergency fund as a financial airbag. You hope you never need it, but if life throws a sudden curveball—a job loss, a major car repair, or an unexpected medical bill—you’ll be incredibly grateful it’s there. Without a clear savings goal, it’s easy to either save too little (leaving yourself vulnerable) or put off saving entirely because the target feels too vague.

In this complete guide, we’ll walk through exactly how to use an emergency fund calculator effectively, what factors influence your target number, and how to build that safety net without feeling overwhelmed. We’ll look at real-world scenarios and practical strategies so you can sleep better knowing you’re prepared.

Why a Standard Emergency Fund Calculator Beats Generic Advice

You’ve probably heard the rule of thumb: save three to six months’ worth of living expenses. While that’s a decent starting point, it’s like saying “wear a medium-sized shirt” without knowing if you’re a petite frame or an athletic build. An emergency fund calculator tailored to your situation accounts for the nuances that generic rules miss.

In practice, the “right” amount varies wildly depending on your job stability, monthly obligations, family size, and even your health. A freelancer with variable income has very different needs compared to a tenured government employee. A single person renting a small apartment has different exposure than a family of four with a mortgage and two car payments.

Based on real use cases I’ve observed while helping friends and family plan their finances, those who used a personalized calculator felt more confident and stuck to their savings goals longer. When you have a specific number in mind—say, $8,400 instead of “a few months of expenses”—it becomes a concrete target you can work toward, month by month.

Professionals working in this area often observe that people who set specific savings goals are far more likely to achieve them. An emergency fund calculator provides that specificity, transforming anxiety about the unknown into a manageable financial plan.

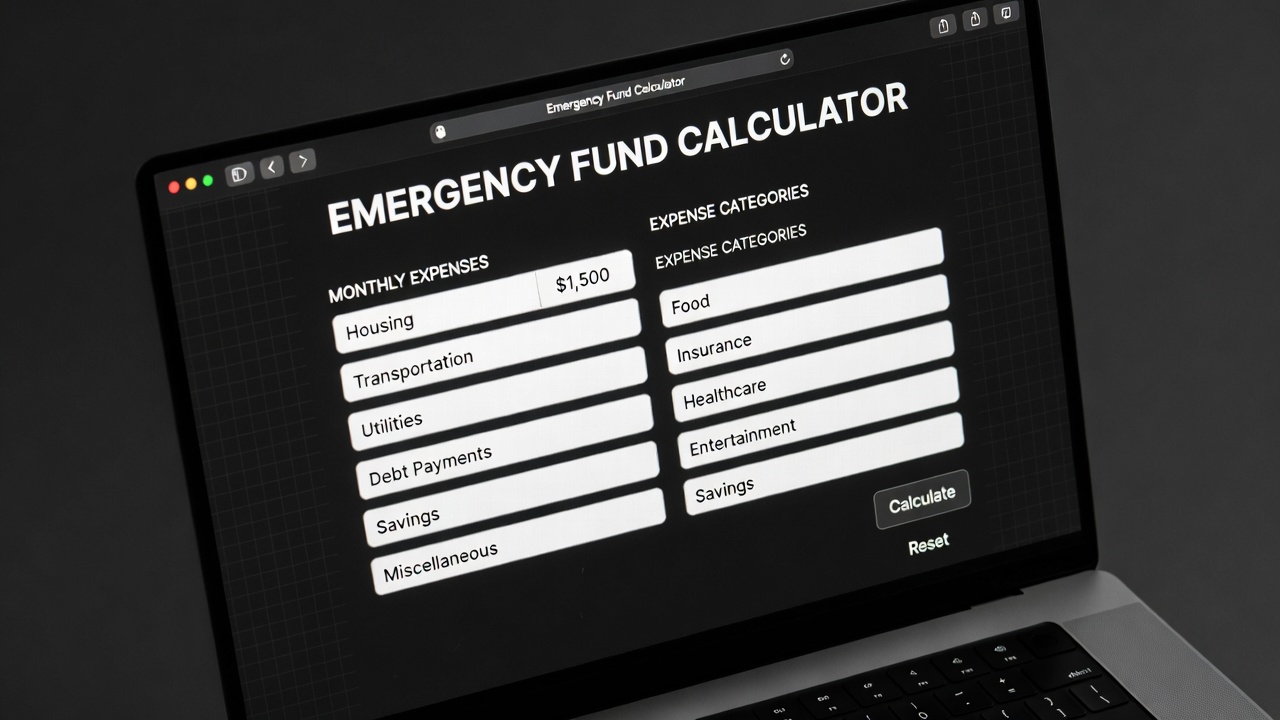

How to Use an Emergency Fund Calculator: A Step-by-Step Approach

Using one of these calculators is straightforward, but the accuracy depends entirely on the information you feed it. Think of it like baking: if you guess at the ingredient quantities, the cake won’t rise. Let’s break down the process so your emergency fund truly fits your life.

- Step 1: Calculate Your Essential Monthly Expenses: This is the core of any emergency fund calculator. You need to separate wants from needs. Essential expenses include rent or mortgage, utilities (electricity, water, gas), groceries, minimum debt payments, insurance premiums, transportation costs (gas or public transit), and basic healthcare. Exclude dining out, streaming subscriptions, and shopping budgets. Be ruthlessly honest here.

- Step 2: Determine Your Risk Profile and Time Horizon: Why does this matter? A dual-income household with stable jobs might feel comfortable with three months of expenses saved. A single-income family or someone in a volatile industry might need six months or even more. Some advanced emergency fund calculators ask about job security, health, and other income sources to adjust the multiplier.

- Step 3: Factor in One-Off Emergency Events: Your monthly expenses cover ongoing costs, but emergencies often come with lump-sum needs. Consider your insurance deductibles for health, home, or auto. If your HVAC system fails or you need a major dental procedure, what’s the out-of-pocket cost? A thorough emergency fund target should include these potential hits.

- Step 4: Do the Math: Multiply your essential monthly expenses by the number of months you want to cover (your risk-based multiplier). Then, add a buffer for those larger, less frequent emergency costs. The formula looks like this: (Essential Monthly Expenses × Coverage Months) + Major Emergency Buffer = Total Emergency Fund Goal.

From hands-on experience, running through these steps often surprises people. Some realize they need less than they feared, which is motivating. Others discover they were underestimating their true vulnerability, which provides crucial clarity. Either way, you’re no longer operating in the dark.

Once you have your target number, you can break it down into smaller, achievable milestones—maybe your first goal is one month’s expenses, then three months, and finally your full target.

Real-World Scenarios: What Emergency Fund Calculations Look Like

Let’s make this concrete with a couple of examples. These aren’t one-size-fits-all, but they illustrate how an emergency fund calculator adapts to different lives.

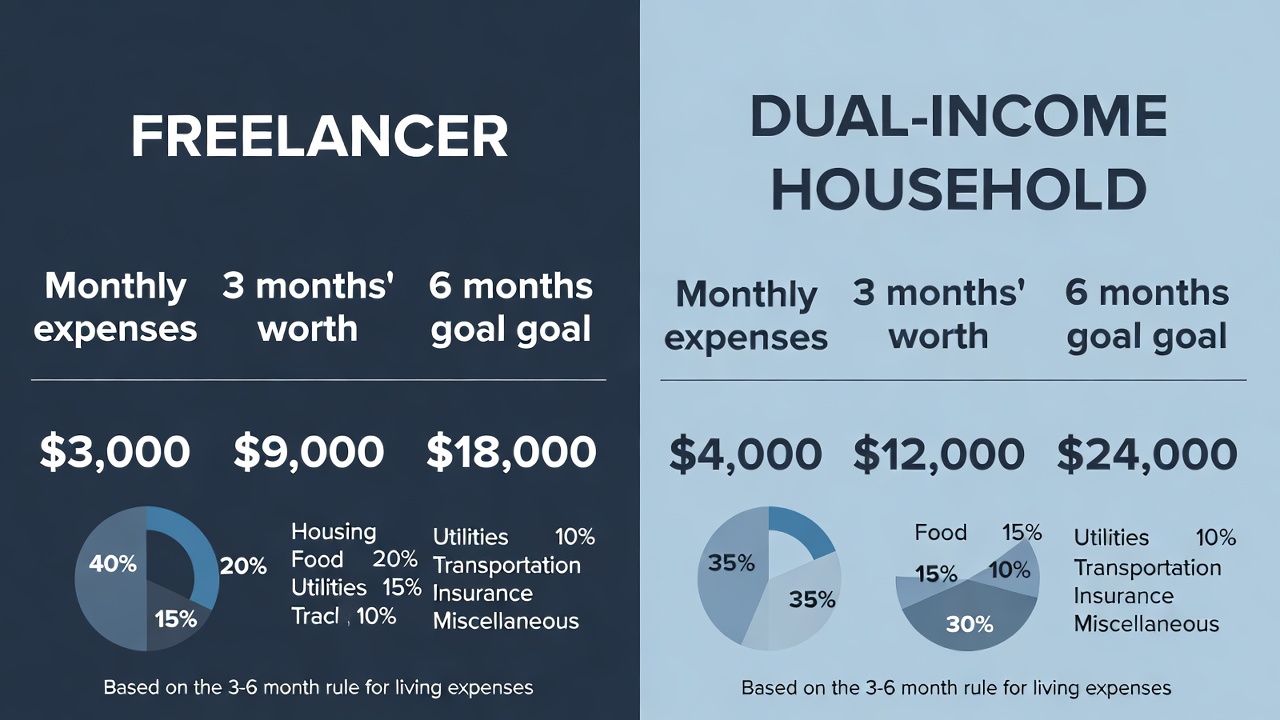

Scenario A: The Freelancer

Maria is a graphic designer with fluctuating income. Her essential monthly expenses are $3,200 (rent, utilities, groceries, insurance, and minimum student loan payments). Given her variable income, she and her financial advisor decide an 8-month cushion is prudent. Her base calculation is $3,200 × 8 = $25,600. She also knows her health insurance deductible is $3,000 and her laptop is essential for work, so she adds a $2,000 buffer for potential replacement/repair. Her total emergency fund goal via the calculator is $30,600.

Scenario B: The Dual-Income Household

James and Priya both work in education with stable jobs. Their essential monthly expenses are $4,500 (mortgage, utilities, groceries, two car payments, daycare). With two incomes and good job security, they opt for a 3-month target. Their base calculation is $4,500 × 3 = $13,500. They have a $1,000 deductible on their home and auto insurance combined, so they add a $1,500 buffer for potential larger expenses. Their total goal is $15,000.

See how different those numbers are? Maria needs over $30,000, while James and Priya need half that, even though their monthly expenses are higher. That’s the power of personalization.

Common Mistakes People Make When Using an Emergency Fund Calculator

Even with a good tool, it’s easy to trip up. I’ve made some of these errors myself, and I’ve seen friends fall into the same traps. Avoiding them makes your emergency fund far more effective.

Mistake 1: Underestimating Essential Expenses: It’s tempting to cut your budget too lean when calculating essentials. You might think “I could cancel my internet if things got tight,” but in reality, internet is essential for job hunting and many daily tasks. Be realistic about what you truly can’t avoid paying.

Mistake 2: Ignoring Irregular but Predictable Expenses: Car registration, semi-annual insurance premiums, or annual subscriptions often get left out of monthly calculations. A better approach is to total these for the year, divide by 12, and add that amount to your monthly essential expenses. This gives a truer picture.

Mistake 3: Treating the Fund as a One-and-Done: Your life changes—you might get a raise, have a baby, or pay off a debt. Your emergency fund target should evolve with you. Revisit the calculator every year or after major life events.

Mistake 4: Keeping the Fund Too Accessible (or Not Accessible Enough): The money needs to be liquid—you can’t have it tied up in stocks that might drop 30% right when you need it. But if it’s too easy to access (like in your everyday checking account), you might dip into it for non-emergencies. A high-yield savings account separate from your main bank account is often the sweet spot. While exact figures may vary depending on context, current rates in high-yield savings accounts are significantly better than traditional savings, helping your fund keep pace with inflation.

These pitfalls are common, but awareness is half the battle. Adjust your approach, and your safety net will be much stronger.

Where to Keep Your Emergency Fund for Optimal Growth and Access

Once your emergency fund calculator gives you a target, the next question is where to park that money. You need a balance of three things: safety, liquidity (easy access), and a reasonable return so inflation doesn’t eat away at your purchasing power.

High-Yield Savings Accounts (HYSA): This is the most popular and often the best choice. These accounts are FDIC-insured (up to $250,000), so your money is safe. They offer much better interest rates than traditional savings accounts, and you can withdraw money quickly, usually within a day or two. From hands-on experience, opening an HYSA online takes about 10 minutes, and it creates a helpful mental barrier—it’s separate from your spending money, reducing temptation.

Money Market Accounts: Similar to HYSAs, they often offer competitive rates and may come with a debit card or check-writing abilities, which can be convenient. They are also FDIC-insured. Just be aware of any monthly fees or minimum balance requirements that could eat into your returns.

Certificates of Deposit (CDs) or Treasury Bills (T-bills): These can be part of a “laddering” strategy for the portion of your fund you’re less likely to need immediately. For example, you might keep two months’ expenses in a HYSA and ladder the rest in 3-month, 6-month, and 12-month CDs. This can lock in slightly higher rates, but you risk penalties if you need to withdraw early. It requires more active management.

What to Avoid: The stock market, cryptocurrency, or any volatile investment. Your emergency fund is not for growth; it’s for protection. Also, avoid stashing it under the mattress or in a standard checking account where it’s losing value to inflation and too easy to spend.

Expert Tips for Reaching Your Emergency Fund Goal Faster

Knowing your number from an emergency fund calculator is one thing; reaching it is another. Here are some practical, battle-tested strategies to accelerate your savings without feeling deprived.

Automate It: Set up an automatic transfer from your checking account to your designated emergency fund savings account every payday. Even $50 or $100 per check adds up faster than you think. “Out of sight, out of mind” works wonders here.

Use Windfalls Wisely: Tax refunds, work bonuses, birthday cash, or side-hustle income can be turbo-boosters. Instead of spending it all, commit to putting a significant percentage—say 50% or more—directly into your emergency fund. You’ll reach your target months or even years sooner.

Cut One Expense and Redirect It: Look at your budget for one non-essential expense you can temporarily pause. Maybe it’s that gym membership you don’t use, or a subscription service. Cancel it and automatically divert that monthly amount to your fund. It’s a small sacrifice with a big payoff.

Start Small and Build Momentum: If the full target feels daunting, focus on your first milestone—$1,000 or one month’s expenses. Achieving that first goal feels great and builds the momentum to keep going. Professionals working in this area often observe that celebrating these small wins is key to long-term financial habit formation.

Remember, building an emergency fund is a marathon, not a sprint. Consistency matters more than the size of each contribution.

Data-Backed Insight: The Real Cost of Not Having an Emergency Fund

It’s easy to think “nothing bad will happen,” but the data tells a different story. According to the Federal Reserve’s Report on the Economic Well-Being of U.S. Households, a significant portion of adults would struggle to cover a $400 emergency expense using cash or its equivalent. This forces many to rely on credit cards, payday loans, or borrowing from friends and family, which can create a cycle of debt that’s hard to escape.

While exact figures may vary depending on context and the year of the survey, the trend is consistent: financial fragility is widespread. Having a fully funded emergency fund isn’t just about convenience; it’s about resilience. It prevents a single setback—like a car breakdown or a minor medical bill—from derailing your entire financial life. It protects not only your bank account but also your credit score and your peace of mind.

This isn’t about fear-mongering. It’s about recognizing that life is unpredictable. An emergency fund is the bridge that gets you safely from “unexpected event” to “back on your feet” without falling into a canyon of high-interest debt.

Conclusion

An emergency fund isn’t the most glamorous part of personal finance, but it is absolutely the foundation. Using an emergency fund calculator to determine your personalized savings target transforms a vague “should do” into a clear, actionable financial goal. We’ve explored how to calculate your essential expenses, factor in your unique risk profile, avoid common mistakes, and choose the right place to park your savings.

The most important takeaway is this: start where you are, use what you have, and do what you can. Whether your target is $5,000 or $50,000, the journey begins with a single automated transfer. That safety net you’re building isn’t just about money; it’s about freedom, resilience, and the confidence to face whatever comes your way.

Take 20 minutes this week to run your numbers through a calculator. It might just be the most productive financial appointment you make all year.

🛒 Recommended Tools for Building Your Emergency Fund

Based on the emergency fund calculator principles discussed in this article, we’ve curated a selection of top-rated products and services that can help you save more effectively and manage your money better. These recommendations are carefully chosen to help you implement the solutions that best fit your needs and budget.

Disclosure: If you purchase through these links, we may earn a commission at no extra cost to you.

Frequently Asked Questions About Emergency Fund Calculators

1. What is an emergency fund calculator, and how does it work?

An emergency fund calculator is a tool (often a simple spreadsheet or online widget) that helps you determine how much money you should save for unexpected expenses. It works by taking your essential monthly expenses, multiplying them by a chosen number of months (based on your job security), and often adding a buffer for large, one-time emergency costs like insurance deductibles.

2. How many months of expenses should I really save?

There’s no single right answer. The classic recommendation is 3-6 months, but it depends on your personal risk factors. Single-income households, freelancers, or those in volatile industries should lean toward 6-9 months or more. Stable dual-income households might be comfortable with 3 months. An emergency fund calculator helps you make this decision based on your specific situation.

3. Should I include discretionary spending like dining out in my calculation?

No. An emergency fund is for survival mode. In a true emergency, you would cut all non-essential spending. Focus on absolute necessities: housing, utilities, food, transportation, insurance, and minimum debt payments. This gives you a leaner, more accurate target.

4. Where is the best place to keep my emergency fund?

A high-yield savings account (HYSA) is generally the best option. It offers safety (FDIC insurance), liquidity (you can access money quickly), and a competitive interest rate to fight inflation. Money market accounts are also a good alternative. Avoid the stock market for these funds.

5. Can I use my emergency fund calculator target even if I have debt?

Yes, but with a strategy. It’s often recommended to build a small starter emergency fund of $1,000 to $2,000 first, then focus on paying down high-interest debt. Once the debt is under control, you can build your fund up to the full calculator target. This approach prevents you from going deeper into debt if a small emergency pops up.

6. How often should I update my emergency fund calculation?

Revisit your calculation at least once a year or after any major life change—a new job, a raise, a marriage, a child, buying a house, or paying off a significant debt. Your expenses and risk profile evolve, and your safety net should too.

7. What if my emergency fund calculator says I need $30,000, but that feels impossible?

Break it down into smaller milestones. Focus on saving one month’s expenses first ($5,000 in this example). Then aim for two months, and so on. Automate small, consistent contributions. It’s a long-term goal, and even reaching a partial target puts you far ahead of most people.

8. Is my emergency fund separate from savings for a house or vacation?

Absolutely. Your emergency fund is not for planned expenses like a down payment, a wedding, or a vacation. It has one job: to protect you in a true financial crisis. Keep it completely separate from your other savings goals to avoid the temptation to dip into it.

- How to Make Money Online 2026

How to Make Money Online 2026: A Practical Guide for Beginners By Sanso Uka Many people are… Read more: How to Make Money Online 2026

How to Make Money Online 2026: A Practical Guide for Beginners By Sanso Uka Many people are… Read more: How to Make Money Online 2026 - Best Side Hustles 2026

7 Best Side Hustles 2026: A Practical Guide to Increasing Your Income By Sanso Uka Finding the… Read more: Best Side Hustles 2026

7 Best Side Hustles 2026: A Practical Guide to Increasing Your Income By Sanso Uka Finding the… Read more: Best Side Hustles 2026 - How to Start a Freelance Career

How to Start a Freelance Career for Long-Term Financial Success By Sanso Uka The idea of being… Read more: How to Start a Freelance Career

How to Start a Freelance Career for Long-Term Financial Success By Sanso Uka The idea of being… Read more: How to Start a Freelance Career - How to Negotiate Salary

How to Negotiate Your Salary in 2026: A Practical Guide for Every Stage of Your Career By… Read more: How to Negotiate Salary

How to Negotiate Your Salary in 2026: A Practical Guide for Every Stage of Your Career By… Read more: How to Negotiate Salary - Emergency Fund Calculator

Author: Sanso Uka Emergency Fund Calculator: How Much You Really Need for Financial Security If you’ve ever… Read more: Emergency Fund Calculator

Author: Sanso Uka Emergency Fund Calculator: How Much You Really Need for Financial Security If you’ve ever… Read more: Emergency Fund Calculator - How to Build an Emergency Fund Faster

How to Build an Emergency Fund Faster Without Sacrificing Your Lifestyle Saving money for a rainy day… Read more: How to Build an Emergency Fund Faster

How to Build an Emergency Fund Faster Without Sacrificing Your Lifestyle Saving money for a rainy day… Read more: How to Build an Emergency Fund Faster - High Interest Deposit Account

Author: Sanso Uka Complete Guide to High Interest Deposit Accounts (2026) If you’ve been wondering where to… Read more: High Interest Deposit Account

Author: Sanso Uka Complete Guide to High Interest Deposit Accounts (2026) If you’ve been wondering where to… Read more: High Interest Deposit Account - High Yield Interest Savings Account

Complete Guide: High Yield Interest Savings Account 2026 Complete Guide: High Yield Interest Savings Account 2026 If… Read more: High Yield Interest Savings Account

Complete Guide: High Yield Interest Savings Account 2026 Complete Guide: High Yield Interest Savings Account 2026 If… Read more: High Yield Interest Savings Account - Highest Interest Rate Savings Account

The Complete Guide to the Best High Yield Savings Accounts in the United States (2026) If your… Read more: Highest Interest Rate Savings Account

The Complete Guide to the Best High Yield Savings Accounts in the United States (2026) If your… Read more: Highest Interest Rate Savings Account - Best High Yield Savings Accounts in the United States

The Complete Guide to the Best High Yield Savings Accounts in the United States (2026) If your… Read more: Best High Yield Savings Accounts in the United States

The Complete Guide to the Best High Yield Savings Accounts in the United States (2026) If your… Read more: Best High Yield Savings Accounts in the United States - Small Business Tax Deductions List

The Complete Small Business Tax Deductions List for 2026 The Complete Small Business Tax Deductions List: 50+… Read more: Small Business Tax Deductions List

The Complete Small Business Tax Deductions List for 2026 The Complete Small Business Tax Deductions List: 50+… Read more: Small Business Tax Deductions List - Starting a Consulting Business

Starting a Consulting Business: Complete Guide to Building Your Independent Practice in 2025 Author: Sanso Uka Starting… Read more: Starting a Consulting Business

Starting a Consulting Business: Complete Guide to Building Your Independent Practice in 2025 Author: Sanso Uka Starting… Read more: Starting a Consulting Business