The Complete Guide to the Best High Yield Savings Accounts in the United States (2026)

If your savings are sitting in a traditional brick-and-mortar bank account, you might be leaving a surprising amount of money on the table. I’ve been there myself, content with the convenience of having my checking and savings at the same well-known bank, only to realize years later that my “savings” were barely growing. It’s a common scenario. You work hard to set money aside, and you want it to be safe, but you also want it to work for you.

That’s where high-yield savings accounts come in. In simple terms, a high-yield savings account (HYSA) is a type of savings account that pays a much higher interest rate—or Annual Percentage Yield (APY)—than a standard one. While the national average savings rate hovers around a meager 0.40% to 0.61% as of early 2026, the best high yield savings accounts in the United States are offering rates several times higher, often between 3.30% and 4.00% or more. This guide will walk you through everything you need to know to find the perfect home for your cash, helping you make an informed decision that fits your financial life.

We’ll look at how these accounts work, why they matter right now, and what features (beyond just a high number) you should be looking for. Whether you’re building an emergency fund, saving for a down payment, or just want a better return on your cash, understanding the landscape of high-yield savings is a crucial first step.

Why the Best High Yield Savings Accounts in the United States Matter Right Now

The economic landscape has shifted dramatically over the last few years. We’ve seen inflation rates fluctuate and the Federal Reserve adjust interest rates in response. For savers, this has created a unique environment. Suddenly, the concept of “risk-free” return actually means something again. From hands-on experience, watching a savings account grow noticeably month over month is far more motivating than seeing it earn a few pennies.

Based on real use cases, people are using these accounts for more than just emergency funds. They are parking cash for short-term goals like a wedding, a home renovation, or even a “fun fund” for travel, knowing that the money is liquid but still earning a competitive yield. Professionals working in this area often observe that the psychological benefit of a growing balance can encourage better saving habits overall. It’s not just about the math; it’s about creating momentum.

In practice, the difference is substantial. On a balance of $15,000, the difference between the national average APY (0.40%) and a high-yield account at 3.60% is about $480 per year. That’s real money that you earn just for moving your savings to a different type of account. It’s essentially free cash with no additional risk, thanks to FDIC insurance.

However, it’s important to remember that APYs are variable. Banks can and do change their rates based on the federal funds rate. While exact figures may vary depending on the broader economic context, the gap between high-yield accounts and traditional ones is likely to persist because online banks have lower overhead costs and pass those savings on to customers.

Key Features to Look for in a High-Yield Savings Account

When you start shopping around, it’s easy to get tunnel vision and only look at the APY. While the interest rate is the headline, the fine print matters just as much for a positive experience. Here are the critical factors I always evaluate:

- Competitive APY: Obviously, you want a rate that’s well above the national average. Look for accounts consistently in the top tiers, but be aware that some banks offer “teaser” rates that drop after a few months. Check the historical rate stability if possible.

- Low or No Fees: This is a dealbreaker. The best high yield savings accounts in the United States charge no monthly maintenance fees. A fee can quickly erase any interest you earn. Watch out for excessive withdrawal fees, though these are less common now.

- Low Minimum Deposit and Balance Requirements: Many excellent online accounts have no minimum to open and no minimum balance required to earn the top APY. This makes them accessible to everyone, whether you’re starting with $50 or $50,000.

- FDIC Insurance: This is non-negotiable. Ensure the institution is FDIC-insured (or NCUA-insured for credit unions), which protects your money up to $250,000 per depositor, per ownership category. It’s the safety net that makes a savings account risk-free.

- User-Friendly Digital Experience: Since these are primarily online accounts, a good mobile app and website are essential. You’ll want easy transfer capabilities, mobile check deposit, and reliable customer service via chat or phone.

- Liquidity and Transfer Speeds: How quickly can you access your money? While they are savings accounts, you might need the funds in an emergency. Check if the account offers an associated ATM card or how long external transfers typically take (usually 1-3 business days).

When I first opened my HYSA, I focused too much on the APY and ended up with a bank that had a clunky interface and slow transfer times. It was frustrating. Now, I prioritize the overall package. A slightly lower rate from a bank with a great app and instant transfers between accounts is often a better trade-off for convenience and peace of mind.

How to Choose the Right Account for Your Financial Goals

Not all savers are the same, and the “best” account depends heavily on what you’re saving for. Let’s break it down by common financial goals.

If you’re building an emergency fund, your priorities should be stability and access. You want an account from a reliable institution where you can park 3-6 months of expenses. The money needs to be separate from your daily spending but accessible within a day or two. A straightforward HYSA with no frills but a solid APY from a well-known online bank is often the best choice here. You don’t need check-writing abilities or a debit card, just a secure place for your funds to grow while staying liquid.

For short-term savings goals like a vacation or a new car in the next 1-3 years, an HYSA is also ideal. The stock market is too volatile for this timeframe, but a savings account offers guaranteed growth. You might prioritize an account that allows you to create sub-savings buckets or goals within the main account. This feature, offered by banks like Ally or Sofi, helps you visually track progress toward multiple goals without opening multiple accounts. In practice, this simple organizational tool can be incredibly motivating.

If you’re looking to park a large sum temporarily, perhaps from a home sale or an inheritance, you’ll want to ensure your total deposits are within FDIC limits. For amounts over $250,000, you might need to spread the money across multiple institutions. You should also look for accounts with no deposit limits or caps on the amount that earns interest. Some banks only pay the high rate on the first $10,000 or $25,000, so read the fine print carefully.

Ultimately, the right account aligns with your habits. If you’re prone to dipping into savings, choose a bank that makes it slightly harder to transfer out, perhaps one without an instantly linked checking account. If you’re disciplined, a fully integrated ecosystem might work perfectly.

Common Pitfalls to Avoid with High-Yield Savings Accounts

Even a great financial tool can lead to frustration if you’re not aware of the common traps. Based on my own journey and conversations with others, here are a few things to watch out for.

Chasing the Absolute Highest Rate. It’s tempting to jump from bank to bank every time you see a rate that’s 0.10% higher. But consider the time and hassle of opening new accounts, changing direct deposits, and waiting for transfers. Often, sticking with a solid, reputable bank that offers a consistently competitive (if not the very highest) rate is a better long-term strategy. Professionals working in this area often observe that rate-chasers tend to earn less over time due to the “inactivity drag” of money in transit.

Ignoring the Fine Print on Fees and Rate Tiers. Some accounts advertise a high rate but only on balances up to a certain limit. Others might require a certain number of debit card transactions or a monthly direct deposit to qualify for the best APY. If those requirements don’t fit your lifestyle, you could end up earning the standard, much lower rate. Always look for the “fine print” disclosures.

Treating It Like a Checking Account. While HYSAs offer great liquidity, they are not designed for frequent transactions. Federal Regulation D, which limited certain types of withdrawals to six per month, was suspended during the pandemic, but some banks still impose their own limits or fees for excessive transactions. Using your HYSA for daily coffee runs or to pay monthly bills could get your account flagged or cost you in fees. Keep a separate checking account for daily spending.

Forgetting About Inflation. It’s crucial to have realistic expectations. Even a great HYSA rate of 4.00% might not fully outpace inflation during some periods. This doesn’t mean an HYSA is the wrong place for your money; it’s still the right place for cash you need in the short term. But for long-term wealth building (10+ years), investing in a diversified portfolio of stocks and bonds is historically the only way to truly outpace inflation. An HYSA is for safety and liquidity, not for maximizing long-term growth.

Practical Tips for Maximizing Your High-Yield Savings Account

Once you’ve opened your account, a few simple habits can help you get the most out of it. Think of it as a tool in your financial toolkit—the more strategically you use it, the better the results.

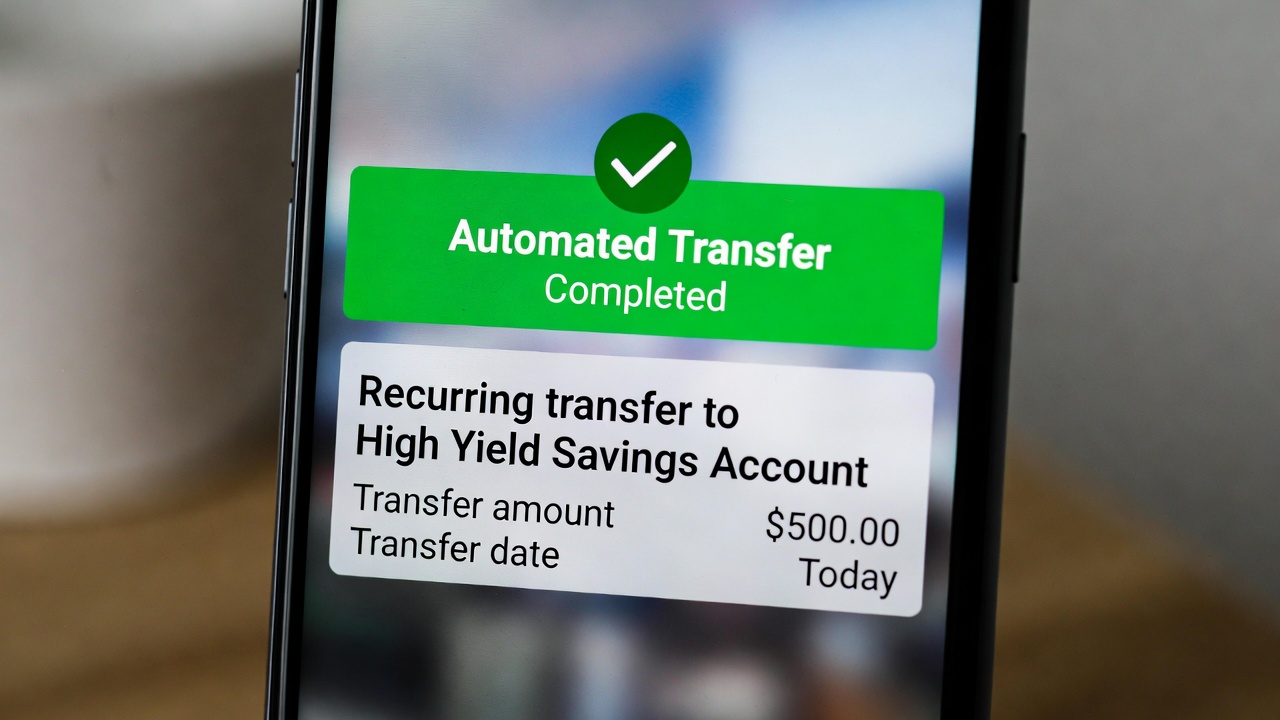

Automate Your Savings. This is the single most effective tip. Set up an automatic transfer from your checking account to your HYSA to coincide with your payday. Even if it’s just $50 or $100, it forces you to “pay yourself first” and makes saving a habit, not an afterthought. You’d be surprised how quickly it adds up, and you won’t miss money you never saw in your spending account.

Use Bonus Offers Strategically. Many banks offer cash bonuses for opening a new account and setting up a direct deposit. This can be a great way to get an extra boost. However, be sure to read the terms, including how long you must keep the account open to avoid fees or clawbacks. Don’t let a one-time bonus lure you into an account with poor long-term value.

Review the Rate Periodically. While you shouldn’t obsess over daily fluctuations, it’s wise to check your account’s APY every 3-6 months. The high-yield savings landscape is competitive, and your bank’s rate might fall behind. A quick check can tell you if it’s time to consider moving to a better option. Websites that track bank rates, like Bankrate or NerdWallet, are useful for this kind of comparison shopping.

Consolidate to Simplify. If you have multiple savings accounts scattered across different banks, consider consolidating them into one or two high-yield accounts. This makes it easier to manage your money, see your total savings picture, and ensure you’re earning a good rate on every dollar. Using a bank with a “bucket” feature can help you maintain mental separation for different goals within one consolidated account.

Online Banks vs. Traditional Banks vs. Money Market Accounts

It’s helpful to understand how HYSAs from online banks stack up against alternatives. This puts their value into perspective.

Online Banks vs. Traditional Brick-and-Mortar Banks: This is the core comparison. Traditional banks (like Chase, Wells Fargo, Bank of America) have massive overhead costs from physical branches. They offer convenience and in-person service, but they pay virtually nothing on savings deposits (often 0.01% APY). Online banks (like Ally, Marcus by Goldman Sachs, Discover) have no branches, so they pass their savings on to you in the form of much higher rates. The trade-off? You can’t walk into a local branch to deposit cash or talk to a teller. For most people, this is an acceptable trade for significantly more interest.

High-Yield Savings Accounts vs. Money Market Accounts (MMAs): This is a closer comparison. MMAs often offer competitive, high-yield rates as well. The main difference is that MMAs sometimes come with limited check-writing abilities and a debit card, making them slightly more flexible than a standard savings account. However, they may also require a higher minimum balance to open or earn the best rate. In practice, for most savers, a top-tier HYSA and a top-tier MMA are very similar. The choice often comes down to whether you want the optionality of writing a check from the account. If not, an HYSA is usually the simpler, more straightforward option.

High-Yield Savings Accounts vs. Certificates of Deposit (CDs): A CD is a time-based deposit. You agree to lock your money away for a set term (e.g., 12 months, 3 years) in exchange for a fixed, and often slightly higher, interest rate. The key difference is liquidity. With an HYSA, your money is always accessible. With a CD, you typically pay an early withdrawal penalty if you need the money before the term ends. CDs are great for money you know you won’t need for a specific period, while HYSAs are for funds that need to remain accessible.

How FDIC Insurance Protects Your Money

One of the biggest reasons people hesitate to bank with an online-only institution is fear about the safety of their money. It’s a valid concern, but the answer is straightforward and robust: FDIC insurance.

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the U.S. government. It was created in 1933 in response to the thousands of bank failures during the Great Depression. Its purpose is to maintain stability and public confidence in the nation’s financial system. In practice, this means that if your FDIC-insured bank fails, the FDIC steps in to protect your deposits.

The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category. This means if you have a single account in your name at an FDIC-insured bank, you are protected up to $250,000. If you have a joint account with another person, you are each insured for up to $250,000 for that joint account, providing a total of $500,000 of coverage for that specific account type at that bank.

To check if a bank is FDIC-insured, you can look for the “FDIC-insured” logo on their website or use the FDIC’s BankFind tool on their official website. For credit unions, the equivalent protection is provided by the National Credit Union Administration (NCUA). So, when you put your money in a high-yield savings account at an FDIC-insured online bank, your money is backed by the full faith and credit of the United States government. It’s just as safe as it would be in a traditional bank across town.

Conclusion

Finding the best high yield savings accounts in the United States for your money is one of the simplest and most effective financial moves you can make in 2026. It’s a low-effort way to earn a significantly better return on your cash without taking on any additional risk, thanks to FDIC insurance. The key is to look beyond just the APY and consider the whole package—fees, minimums, digital experience, and how the account fits with your specific savings goals.

Start by identifying what you’re saving for. Is it a rainy day fund, a dream vacation, or a down payment? Then, use the criteria we’ve discussed to compare a few reputable online banks. Remember to automate your savings to build momentum effortlessly. A high-yield savings account isn’t a get-rich-quick scheme; it’s a smart, foundational tool for building financial stability and making your hard-earned money work just a little bit harder for you, every single day.

🛒 Tools to Manage Your High-Yield Savings Journey

Based on the best high yield savings accounts in the United States discussed in this article, we’ve curated a selection of top-rated financial apps and resources that can help you track your savings goals, compare rates, and automate your finances. These tools are designed to complement your savings strategy and help you stay on track.

Frequently Asked Questions About High-Yield Savings Accounts

Are high-yield savings accounts safe?

Yes, as long as they are held at an FDIC-insured bank (or NCUA-insured credit union). Your deposits are protected up to $250,000 per depositor, per ownership category. This makes them one of the safest places to park your cash.

Can I lose money in a high-yield savings account?

You cannot lose the principal amount you deposit, provided you stay within FDIC limits. The only potential “loss” is purchasing power if the interest rate is lower than inflation, but your nominal dollar balance will not decrease.

How is interest paid on a high-yield savings account?

Interest is typically calculated daily and paid monthly. You’ll see it deposited directly into your savings account, where it begins earning interest itself, effectively compounding your returns.

Is there a catch with high-yield savings accounts?

There’s no catch, but there are trade-offs. Most HYSAs are offered by online banks, so you won’t have access to physical branches. Rates are also variable, meaning they can change based on the federal funds rate and the bank’s policies.

How many high-yield savings accounts should I have?

It depends on your needs. You can have multiple accounts for different goals, but managing them can be cumbersome. Many modern banks offer “bucket” features within a single account, which is often a simpler solution.

Do I pay taxes on the interest earned?

Yes, the interest you earn in a savings account is considered taxable income by the IRS. You will receive a Form 1099-INT from your bank if you earn more than $10 in interest during the year, and you must report it on your tax return.

What is the difference between APY and interest rate?

APY stands for Annual Percentage Yield. It includes the effect of compound interest, showing the total amount you will earn in a year. The “interest rate” is the base rate without compounding. APY is the more accurate number to use when comparing accounts.

Can I link my high-yield savings account to my current checking account?

Absolutely. Most online banks make it easy to link to external accounts at other financial institutions. This allows you to easily transfer money back and forth electronically, typically taking 1-3 business days.

What happens if my bank goes out of business?

If your FDIC-insured bank fails, the FDIC will step in. In most cases, it arranges for another bank to take over the accounts, and you will have uninterrupted access to your insured funds. If that doesn’t happen, the FDIC will send you a check for your insured deposits.

Are credit unions a good alternative for high-yield savings?

Yes, credit unions can be excellent alternatives. They often offer High-Yield Savings accounts, sometimes called “share accounts” or “money market accounts.” They are insured by the NCUA, which provides the same $250,000 protection as the FDIC.

- How to Make Money Online 2026

How to Make Money Online 2026: A Practical Guide for Beginners By Sanso Uka Many people are searching… Read more: How to Make Money Online 2026

How to Make Money Online 2026: A Practical Guide for Beginners By Sanso Uka Many people are searching… Read more: How to Make Money Online 2026 - Best Side Hustles 2026

7 Best Side Hustles 2026: A Practical Guide to Increasing Your Income By Sanso Uka Finding the right… Read more: Best Side Hustles 2026

7 Best Side Hustles 2026: A Practical Guide to Increasing Your Income By Sanso Uka Finding the right… Read more: Best Side Hustles 2026 - How to Start a Freelance Career

How to Start a Freelance Career for Long-Term Financial Success By Sanso Uka The idea of being your… Read more: How to Start a Freelance Career

How to Start a Freelance Career for Long-Term Financial Success By Sanso Uka The idea of being your… Read more: How to Start a Freelance Career - How to Negotiate Salary

How to Negotiate Your Salary in 2026: A Practical Guide for Every Stage of Your Career By Sanso… Read more: How to Negotiate Salary

How to Negotiate Your Salary in 2026: A Practical Guide for Every Stage of Your Career By Sanso… Read more: How to Negotiate Salary - Emergency Fund Calculator

Author: Sanso Uka Emergency Fund Calculator: How Much You Really Need for Financial Security If you’ve ever wondered… Read more: Emergency Fund Calculator

Author: Sanso Uka Emergency Fund Calculator: How Much You Really Need for Financial Security If you’ve ever wondered… Read more: Emergency Fund Calculator - How to Build an Emergency Fund Faster

How to Build an Emergency Fund Faster Without Sacrificing Your Lifestyle Saving money for a rainy day is… Read more: How to Build an Emergency Fund Faster

How to Build an Emergency Fund Faster Without Sacrificing Your Lifestyle Saving money for a rainy day is… Read more: How to Build an Emergency Fund Faster - High Interest Deposit Account

Author: Sanso Uka Complete Guide to High Interest Deposit Accounts (2026) If you’ve been wondering where to park… Read more: High Interest Deposit Account

Author: Sanso Uka Complete Guide to High Interest Deposit Accounts (2026) If you’ve been wondering where to park… Read more: High Interest Deposit Account - High Yield Interest Savings Account

Complete Guide: High Yield Interest Savings Account 2026 Complete Guide: High Yield Interest Savings Account 2026 If you’ve… Read more: High Yield Interest Savings Account

Complete Guide: High Yield Interest Savings Account 2026 Complete Guide: High Yield Interest Savings Account 2026 If you’ve… Read more: High Yield Interest Savings Account - Highest Interest Rate Savings Account

The Complete Guide to the Best High Yield Savings Accounts in the United States (2026) If your savings… Read more: Highest Interest Rate Savings Account

The Complete Guide to the Best High Yield Savings Accounts in the United States (2026) If your savings… Read more: Highest Interest Rate Savings Account - Best High Yield Savings Accounts in the United States

The Complete Guide to the Best High Yield Savings Accounts in the United States (2026) If your savings… Read more: Best High Yield Savings Accounts in the United States

The Complete Guide to the Best High Yield Savings Accounts in the United States (2026) If your savings… Read more: Best High Yield Savings Accounts in the United States - Small Business Tax Deductions List

The Complete Small Business Tax Deductions List for 2026 The Complete Small Business Tax Deductions List: 50+ Write-Offs… Read more: Small Business Tax Deductions List

The Complete Small Business Tax Deductions List for 2026 The Complete Small Business Tax Deductions List: 50+ Write-Offs… Read more: Small Business Tax Deductions List - Starting a Consulting Business

Starting a Consulting Business: Complete Guide to Building Your Independent Practice in 2025 Author: Sanso Uka Starting a… Read more: Starting a Consulting Business

Starting a Consulting Business: Complete Guide to Building Your Independent Practice in 2025 Author: Sanso Uka Starting a… Read more: Starting a Consulting Business